If you’re ready to purchase a home then one of the first considerations you might have to deal with is a mortgage, often known as a home loan. You’ll find many mortgage bankers and mortgage brokers in Chicago that are willing to offer their services.

But before you decide to take the plunge and speak to one of these companies, it’s vital that you learn more about the process so that you get a better understanding of how the mortgage process works. You’ll learn what’s involved on closing day and if there are any potential pitfalls that you could avoid.

Preparation is the most important component of a successful home purchase. There are numerous options available such as detailed articles on the mortgage process, online mortgage applications, and mortgage calculators that will help you through the entire process.

It’s good to understand the options you have available and which ones are best suited for your personal circumstances. So without further ado, let’s take a look at the dos and don’ts of the mortgage process.

Do’s & Don’ts During The Mortgage Process

Do’s & Don’ts During The Mortgage Process

1. Pre-Qualification and Pre-Approval

✅Do perform an initial mortgage pre-qualification to get a rough estimate of how much you can afford. This is often done through an online mortgage application and you’ll need to provide documents that support your application.

This process is to ensure that once you find a home that you like, you can make a stronger application with a higher chance of success because your lender has already approved that you are able to afford a home in a certain price range. This will also help you figure out what type of home you can afford so that you know the correct price range to aim for.

❌Don’t start looking around for a home until you are pre-approved. The pre-approval process is vital for helping you set a budget, so the last thing you want is to look for a home that you think you can afford, but in reality, it’s completely out of your budget.

This is a mistake that many people make when looking to purchase a new home. On the bright side, it could reveal that you actually have a larger budget than you initially assumed.

2. Financial Decision Management

✅Do prepare a savings plan to mitigate financial issues. Nobody likes unexpected costs so it’s important to have a savings plan in place so that you can pay for your deposit, your mortgage repayments and also larger purchases that you have planned for.

Keeping a budget and financial record of your expenses can help you create a savings plan that will ensure you have enough money to satisfy your lenders.

❌Don’t make large unplanned purchases that could drastically change your savings plan. It’s not every day that we decide to shell out a huge sum of money for something, but you should do your best to avoid making big purchases and accumulating more debts and applying for more loans.

Affecting your credit rating could have negative consequences for your mortgage application so make sure you avoid any large purchases especially if they’re on credit and not with the money in your bank account.

If you absolutely have to make a large purchase for something important, then make sure it’s a planned expense that is detailed in your savings plan so you know how to work around it.

3. Credit Score Rating

✅Do think smart about your current credit rating and continue to improve your credit rating when possible. The last thing you want to do is ruin your credit rating with more loans or by ignoring inaccuracies within your credit report. Make sure you request a copy of your credit report and focus on resolving any issues that may be outstanding or incorrect to ensure that lenders see an up-to-date and corrected version of your current credit rating.

❌Don’t do anything that could compromise your current credit rating score. This involves taking out new lines of credit, making large purchases before submitting your online mortgage application or making late payments for utilities, rent, and other purchases.

This could potentially lower your credit rating score and it will cause your mortgage broker to think twice about accepting an agreement with you.

4. Questions

✅Do remember that you can ask questions to your mortgage banker or mortgage broker. Questions are appreciated by mortgage lenders because it shows that you’re willing to go the extra mile in understanding how the mortgage process works.

If you’re working with a mortgage banker or mortgage broker in Chicago, then it’s important to ask as many questions as you need to feel comfortable during the loan process. It may seem like a difficult task but what’s important to your mortgage representative is that you feel confident and knowledgeable in your decisions all the way till closing day.

❌Don’t overwhelm yourself by trying to understand everything on your own. There are plenty of resources available on the internet that will teach you about the mortgage process, but it’s always better to speak to someone in the industry such as your mortgage advisor.

It can feel overwhelming trying to understand all of the complex technical terms involved and it will only make things more difficult in the long run.

5. Financial Stability

✅Do ensure that you have a stable job and sources of income before purchasing your home. Stability is one of the key factors in the loan process because if you can’t show that you have a stable income, you’re less likely going to have your new loan approved.

It may take longer to process your online mortgage application and you may even be rejected if your income isn’t stable enough.

❌Don’t try to make drastic changes to your lifestyle or employment status. This means quitting your job or changing your career path shortly before purchasing a home. This raises red flags and can cause some major setbacks and slowdowns during the whole mortgage process.

However, the exception to this rule would be if you have a positive employment change, such as being promoted to a higher position or starting up a new business or stream of income. In this situation, your mortgage application won’t be affected negatively.

6. Changes in Income or Lifestyle

✅Do keep documentation regarding any income or lifestyle changes. This extra step will ensure that you can prove any changes in your life such as marital status and changes in your household size or income.

In most cases, this should include payments, statements, money deposits and also other documentation that your lender might request from you. These documents are important on the closing day because it will allow your lender to finalize their offer.

❌Don’t make large changes to your income, lifestyle or bank without having a record of it. Mortgage lenders don’t like it when they are sudden and difficult-to-explain changes made to your accounts or lifestyle.

For instance, if you suddenly deposit a large sum of money then your mortgage broker may find that it’s a strange or questionable sum of money. As long as you have a paper trail that explains the lump sum (such as a paycheck) then it will help in the long run.

Don’t be surprised if your mortgage broker asks for additional records that they didn’t mention previously. You should be prepared enough that you always have documents available to prove any changes that you’ve made in your life or related to your financial situation.

7. Take Help from Experts

✅Do hire assistance and work with professionals when purchasing a home. This is to ensure that you get all of the legal help required and it ensures that you don’t miss anything in the documents provided to you during the mortgage process and on closing day.

There are plenty of mortgage bankers and mortgage brokers in Chicago that you can hire for assistance and there are plenty of online resources to assist you in the process of purchasing your first home.

❌Don’t try and do everything yourself. There are plenty of people that make the mistake of trying to save money by refusing to hire any kind of professionals to assist them, but this can end up being a poor choice because they might miss crucial documents, they might take too long responding to certain requests by the seller and it could be more costly in the long run.

Conclusion

Hopefully, this article has shown you some useful information on how you can better prepare for the mortgage process. The takeaways from this are that you should always have records for anything related to your finances including career changes, pay raises and changes in your household.

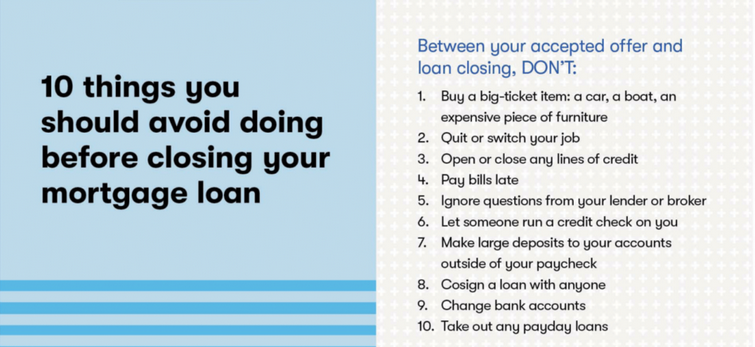

You should also not be afraid to contact people for assistance because the mortgage process can be rather difficult to understand without a trained professional helping you. We’ve also included a downloadable flyer that will explain 10 things that you should avoid doing before closing your mortgage loan. It’s a convenient flyer that will serve as a checklist of things to avoid before the closing day so that you don’t run into any unexpected roadblocks.

For more impartial advice on the mortgage process, then don’t hesitate to check out our own mortgage resources page for more information.

A and N Mortgage Services Inc, a mortgage banker in Chicago, IL provides you with high-quality home loan programs, including FHA home loans, tailored to fit your unique situation with some of the most competitive rates in the nation. Whether you are a first-time homebuyer, relocating to a new job, or buying an investment property, our expert team will help you use your new mortgage as a smart financial tool.