Finding out that your mortgage application has been rejected is one of those heart-sinking moments. You may feel frustrated and upset. You may assume that your property dreams are over for now. You may also be feeling completely perplexed. These feelings are natural.

Understanding why your mortgage application was denied is important. By doing so, you can then make the required changes to make sure it does not get rejected the second time around. Below, we are going to take a look at some of the reasons why your mortgage application may have been denied as well as provide some tips on how to make sure this does not happen.

Possible Reasons Why Mortgage Applications Are Denied

Possible Reasons Why Mortgage Applications Are Denied

Here are some of the main reasons why mortgage applications are denied.

Poor Credit History

There are a number of different reasons why you may have a poor credit rating and this can often be the most worrying reason why your application was denied. A low credit score could be the result of:

- History of late payments – Late payments usually show on your account for seven years. Some mortgage lenders will be willing to lend if you can explain the late payments and prove that you won’t be late on your mortgage repayments.

- Too much debt – Paying this off before you submit your next mortgage application comes highly recommended.

- New credit account – This could be from opening a new credit card account to buy new furniture, clothing or some other reason. This new credit account will show up on your credit report for six months, so it’s a good idea to wait for six months before applying again.

- Too many credit applications – Repeatedly applying for credit indicates that you are relying on credit and that you are desperate to open credit accounts. It is preferable to do soft searches for credit. Hard searches, which show on your credit report, have a negative impact and stay on your credit report for six months.

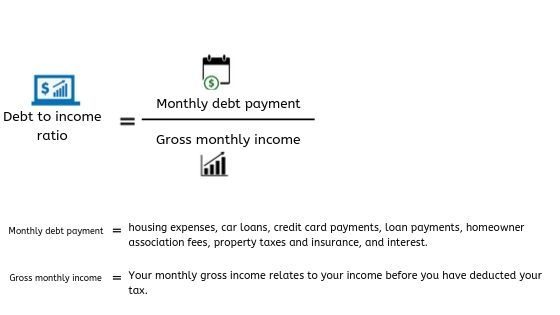

Debt-To-Income Ratio

Another reason why your mortgage application may have been denied is if you have too much debt. Ensuring your debt is at a manageable level is necessary when it comes to building the foundations of good financial health. To assess your debt level, you should consider your debt-to-income (DTI) ratio. What is this? Well, this compares your monthly gross income and your monthly debt expenses.

To work this out, you should add up all of the debt payments you make per month. This includes housing expenses, car loans, credit card payments, and any other debts, for example, loan payments. You also need to add up any homeowner association fees, property taxes and insurance, and interest. This then needs to be divided by your monthly gross income. Your monthly gross income relates to your income before you have deducted your tax. This will give you your debt to income ratio. Most people will then multiply this by 100 so that it is shown as a percentage.  For example, let’s say you make debt payments of $3,000 per month, and your gross income is $5,000, your debt-to-income ratio is 60%. The maximum debt-to-income ratio a lender is willing to accept will, of course, differ from lender-to-lender. However, in most cases, it tends to be around 36%.

For example, let’s say you make debt payments of $3,000 per month, and your gross income is $5,000, your debt-to-income ratio is 60%. The maximum debt-to-income ratio a lender is willing to accept will, of course, differ from lender-to-lender. However, in most cases, it tends to be around 36%.

How To Avoid Mortgage Application Errors?

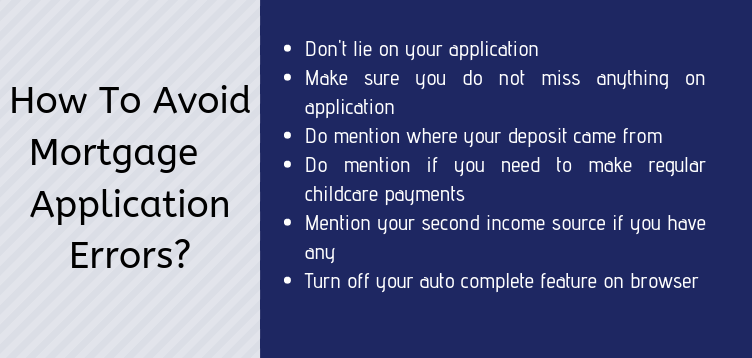

You may have also received notification that your mortgage application has been denied due to the fact that there were errors on your application. Whether the errors were intentional or not, they can really hinder your chances of securing a loan. Leaving information out or failing to complete your mortgage application in full will result in your application being denied.

One thing you should never do is lie on your application. Some people do this because they think that a little white lie will not matter. However, lenders will check the information that you provided and they will often require evidence. If they find out you have lied, your application will be declined.

Depending on the nature of the misstatement, you could even find yourself being prosecuted for fraud. Some of the common lies people make include stating you will live in the house yourself but really you intend to rent it out, saying you have a full-time job when you do not, saying you earn more than you really do or claiming to have a larger deposit than you actually have.

You also need to be very careful in terms of your mortgage application and the number of expenses you have per month. For example, looking after children can be expensive, and so lenders will also consider the cost of this, as well as how much you earn and your other expenses. Make sure your mortgage application is filled in carefully. This is especially important if you complete an application online. Some people have had their applications rejected because of the auto-complete feature on their browser, which led to the wrong information being inputted.

You also need to make sure you do not miss anything from your application, as this could mean your application is rejected, or at best, it could delay your house purchase. Things you should not forget to include are:

- Where your deposit came from, for example, if it was a gift or you saved it yourself

- If you need to make regular childcare payments

- If you moved within the last three years, the lender will need your old address

- If you have a second job, as extra income can help your likelihood of securing the loan

Change In Job Status Affect Mortgage Application

Last but not least, stability is important when it comes to mortgage applications. If you have recently changed your job or lost your job, this could make your lender nervous. This is especially the case if you change your job on a regular basis. Instead, working for the same employer for the past two years or longer can assist with your loan application.

If you have just started a new job, you may boost your chances of being accepted for a mortgage if you submit a number of pay stubs or you ask your current employer to submit your offer letter. If you work as a freelancer or contract worker, you may find it harder to find a mortgage. This does not mean it is impossible. It is all about proving that you have a stable income, so you need to show that you have a consistent amount of money coming in on a monthly basis.

What Are The Next Steps?

- Find out why your application was denied – Get in touch with your lender and find out exactly why your mortgage application was denied. You won’t be able to rectify the issue if you do not know what it was, to begin with.

- Improve your DTI ratio – By now, you should have figured out what your debt-to-income ratio is. You should work on improving this so that you can improve your odds of qualification. There are two ways to reduce your DTI ratio. The first is to improve the income you have coming in every month. The second is to lower the expenses you have going out every month. Some options include paying off loans and credit cards, getting student loans deferred, asking for lower rates from your credit card companies, and refinancing high-interest debt.

- Speak to other lenders – There are many different mortgage lenders. Just because this lender refused your application does not mean another lender is going to do the same. This does not mean you should dive right in and make applications everywhere, though. Speak to lenders to evaluate your choices before taking any steps forward.

- Consult a Mortgage Banker or Mortgage Broker –Finally, a mortgage broker can assist because they will be able to point you in the direction of loans that are right for you. For example, if you are a freelancer, they may know lenders who are more accepting of freelancers and contractors.

Most Trusted Mortgage Bank In Chicago: A and N Mortgage

A and N Mortgage has a reputation as being one of the most trusted mortgage banks in Chicago. If you would like to discuss your options if your first mortgage application is denied, please do not hesitate to get in touch with us today for more information. You can even apply online here and browse the helpful mortgage tools on our website.

A and N Mortgage Services Inc provides you with high-quality home loan programs, including FHA home loans, tailored to fit your unique situation with some of the most competitive rates in the nation. Whether you are a first-time homebuyer, relocating to a new job, or buying an investment property, our expert team will help you use your new mortgage as a smart financial tool.